B2B software as a service, or SaaS, founders entered 2020 riding a wave of the longest economic expansion in United States history. Valuations increased to new highs, funding rounds continued getting larger at each stage, and forecasts went up and to the right fast. But then, March hit.

Quickly and seemingly out of nowhere, headlines became dominated by apocalyptic predictions of death, record levels of unemployment, shocking economic forecasts of GDP contraction, historic mass layoffs and furloughs, and unprecedented multi-trillion dollar economic stimulus packages. For founders every instinct began screaming to cut costs and hunker down.

But should B2B SaaS founders cut their organizations right now? Through analyzing a few key events and looking to the evidence in the market today, founders can develop a strategy for growing during this crisis. Not only is growth cheaper for most B2B SaaS against the backdrop of economic meltdown, but with the majority following a hunker-down instinct, a growing B2B SaaS firm will compare very favorably against a landscape of stale and stagnant competitors.

Reviewing the 1918 Spanish Flu Pandemic and the 2008 downturn

While the health implications vary widely between the current pandemic and the 1918 flu epidemic, the economic reactions share many similarities. The US response to 1918 was just as fractured as the states' reactions to COVID have been this year. As cities and states in 1918 shut down commerce to stem the spread of the flu, economic contraction quickly gave way to rebound, the so called "V-shaped recovery," despite the Spanish Flu having much higher death rates among working individuals than COVID-19.

There are major differences between 1918 and 2020, however. First, there is untapped potential in technology to replace workers. As businesses look for ways to cut costs, expect them to aggressively turn to automation, ultimately depressing real wages. Second, the 1918 response did not include shutdown measures as draconian as those we are experiencing in 2020. This could lead to permanent output loss across a wide range of industries, increasing real prices just as real wages decline. And third, the trillions of dollars in federal economic relief are unlike anything attempted in 1918.

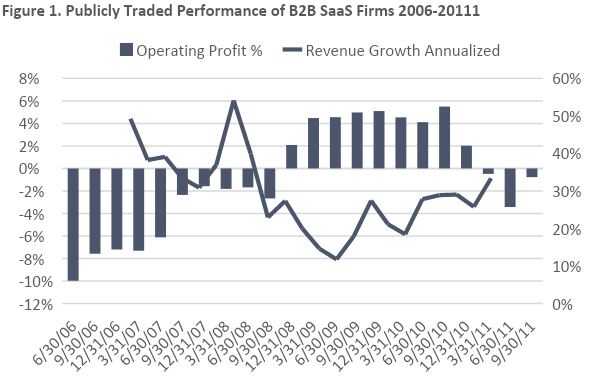

The 2008 downturn that nearly brought the financial sector to a halt rippled through the economy as businesses in a wide range of industries made steep cuts to operations and capital expenditures. Despite this dangerous environment, SaaS firms increased profitability and continued to grow revenues each quarter. Growth slowed but remained positive while most other companies experienced absolute declines in revenue.

Customer acquisition for SaaS businesses usually gets more efficient during downturns, driving the potential for faster growth. The performance of all publicly traded B2B SaaS firms during 2008 illustrated in Figure 1 above proves the resilience of this category during a recession. While revenue continued to grow, profitability rose from a 10 percent loss on average to a 5 percent gain on average by 2010. This is likely due to firms freezing salaries and hiring and perhaps cutting down the sales and marketing budgets.

Downturn case study: Salesforce

Salesforce entered the downturn as a category leader in B2B SaaS with nearly $500M in revenue in 2007 and $3.5 million in operating losses. Throughout 2008, the company grew revenues by 51 percent to $748 million and operating profit surged to $20.3 million. And in 2009, the company repeated this stellar performance by growing revenues 44 percent to $1,077M and operating profit to $63 million. These results occurred against the backdrop of a global financial downturn and with a product focused on helping people sell more effectively (not something one would expect would sell well during a free-fall recession).

The revenue growth throughout those years followed the growth in sales and marketing spend. In 2008, the company grew sales and marketing by 49 percent, driving 51 percent revenue growth at about $1.50 of sales expense per $1 of recognized revenue added. In 2009, the company grew sales and marketing 42 percent resulting in 44 percent revenue growth at $1.63 of sales expense per $1 of recognized revenue. By 2010, the sales growth advantage was gone and Salesforce not only dropped its expense growth rate but also reverted to spending $2.64 per $1 of new revenue added.

Looking at these results Salesforce executed on the growth opportunities in 2008 and 2009 by ramping up sales expenses. The relative cost to acquire customers in 2008 and 2009 compared to 2010 proved significantly cheaper (approximately 40 percent less expensive). When faced with an advantage like that, every founder should charge ahead.

------

Dougal Cameron is director of Houston-based Golden Section Venture Capital.