For has long as I can remember, I had to live near water. That's why I moved to Houston. Recently, new neighbors moved next door from the downtown Galleria area. They loved it there until coronavirus turned shopping habits into stay-at-home habits. The experience led them to recognize they could do just fine without the Galleria-area routine, pivoting instead to a maritime lifestyle.

Could COVID-19 be triggering an inversion paradigm? An inversion paradigm puts needs first rather than product first. We have experienced many historic technology inversions. Remember when our televisions were air-wave dependent and telephones were tethered to the wall? Because the need evolved for a phone that was mobile, today our TV's are wired, and our telephones are untethered.

This technology inversion fundamentally found its way to the individual consumer and transformed entire industries. Houston businesses are responding to a rare COVID-19-induced disruption. Inversions are rare, but when they occur, opportunity follows.

Large infrastructure challenges are normally led by bureaucratic funding processes that result in productized solutions. Hurricane Harvey was a wake-up call to take decisive action to protect decades of private and public investment against future flood events. It was an analogue to removing the board with the nail in it from the driveway to avoid endless tire repairs.

Now, Houston's resilience infrastructure is going through a Hurricane Harvey-induced inversion. The fundamental approach to water management is experiencing a historic reversal which focuses on need rather than a response cycle. Largely dependent on surface run-off systems, Houston experienced a river running through it during Hurricane Harvey. In response, studies and projects are underway to consider a major underground storm drainage system. Water management is fundamentally changing to move stormwater from above ground to below grade, while domestic water is moving away from underground sources to surface supplies, such as lakes. These programs reduce threats to downtown, allowing urbanism and businesses to flourish, simply by addressing a human need in lieu of building another drainage product.

Fortunately for the Houston economy, pre-COVID, quasi-inversion programs already in place to address mobility needs, such as the $7.5 billion METRONext program and $4.8 billion for flood control essentials, are injecting billions of dollars into the local economy. At the federal level, future stimulus funding designed to address infrastructure needs and the economic impact of Coronavirus are likely to follow next year. Consequently, the current Hurricane Harvey, COVID-19 inversion could position Houston to rebound from a time of trial reimagining what a next generation city in the modern age should look like.

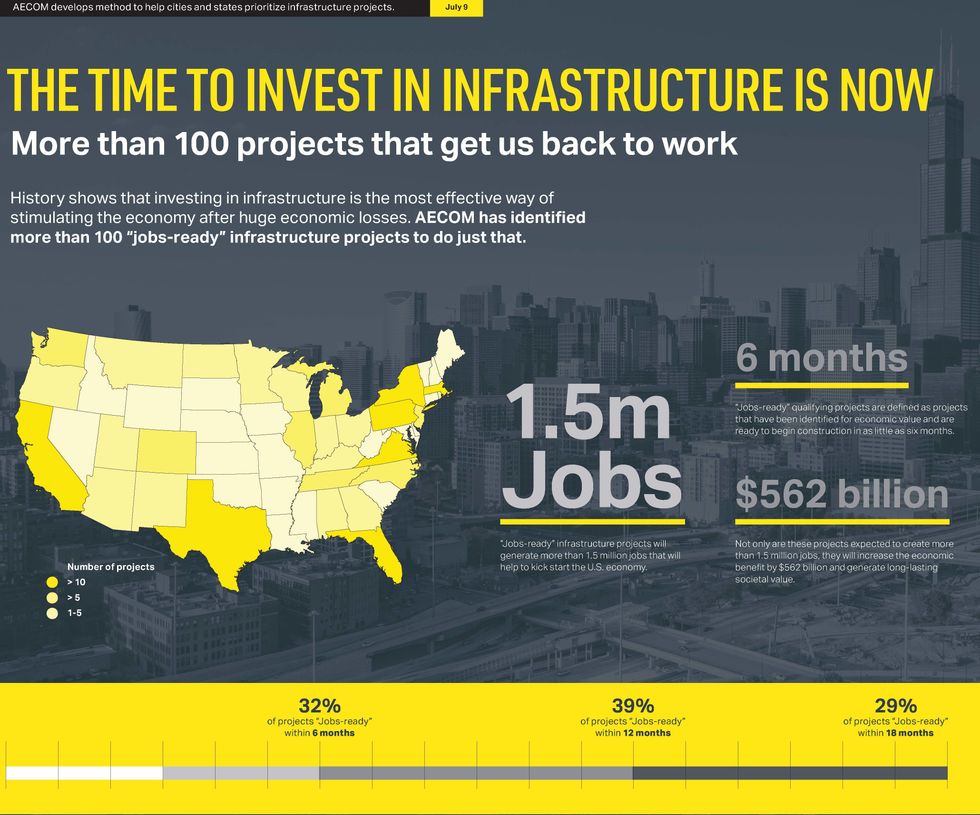

Graphic courtesy of AECOM

Graphic courtesy of AECOM

In fact, infrastructure programs have a long history of creating sustainable jobs and transforming cities. Did you know the River Walk in San Antonio, a downtown centerpiece that thrives today and contributes to thousands of job opportunities, was a construction project born during the Great Depression to address a disastrous flood occurring in the early 1920s? San Antonio architect Robert H. H. Hugman was elected to address a need to save lives and reimagine San Antonio's downtown. The city was altered forever by creating a flood resilience infrastructure that also transformed its city center into a civic gathering place that made San Antonio one of the largest destination cities in Texas.

While technology inversions are occurring more often than before, they are still rare, and each one is very important. Infrastructure inversions that transform cites are even more exceptional. In a COVID-19-induced inversion period, the possibilities are limitless, and the time is now. With programs underway and potential stimulus funding to support additional investment to address city needs, Houston is positioned for something amazing.

------

Tony Loyd is based in Houston and vice president at AECOM.